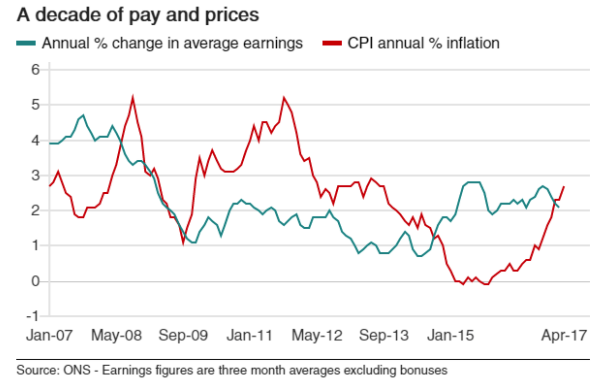

A recent national report conducted by the Office of National Statistics (ONS) has revealed that wages are increasing at a slower rate than inflation for the first time since 2014. Right now, the average salary has increased by 2.1% in the three months to March; however, inflation is up 2.3% over the same time period, creating a differential of -0.2%.

Simply put, the average cost of living is currently rising at a faster rate than real wages, which means that people now have less disposable income after paying for their weekly and monthly essentials. Experts say that the current trend can be attributed to the longer term impact of Brexit on UK households and their total budget.

The below graph is a good visualisation of the current trend, and shows the correlation between average earnings and inflation (CPI) over the last 10 years:

Unemployment lower than ever – but is it all good news?

Also this week, the ONS announced findings that the UK unemployment rate was the lowest it’s been for 42 years. Currently, there are approximately 31.95 million people in work, which works out to around 75% of 16 to 64-year olds.

It’s clear that Britain’s businesses are now hiring more employees than at any other point in recent memory; the problem is that the average job cannot be considered ‘well-paid’ in the context of our current cost of living. Again, the general thought among economists is that this trend is only temporary, and it won’t be long before real wages start rising in line with the demand for employment.

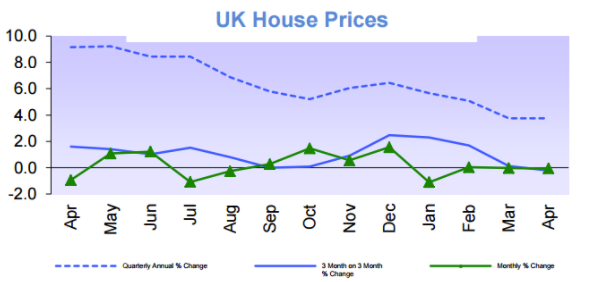

According to a recent statement released by Halifax, house prices in the three months to April 2017 were approximately 0.2% lower than in the previous quarter. That means the average house price now stands at £219,649. Although the fall may seem marginal enough, this is actually the first quarterly decline in the UK housing price index since November 2012.

The report follows another statement made by Nationwide last week that revealed house prices were, in fact, growing at a slower annual rate than at any other time during the last four years – a relatively sluggish 2.6% growth per year, to be exact.

Both reports are indicative of a general downward trend emerging in the property market in the first half of 2017:

Why are house prices stagnating?

The fall in house prices reflects the current demand for housing, which seems to have been falling in recent months due to affordability.

If you consider that until this point house prices have been consistently inflating each quarter for nearly five years, it seems that now we’ve finally reached a tipping point – albeit a modest one. Simply put, the cost of reaching the next rung on the property ladder has inflated beyond what most people can afford.

Supply is also a major factor. A recent RICS report revealed that the average stock levels on estate agents’ books is at a historic low, which means there are fewer options than ever for people looking to move.

Nevertheless, mortgage rates remain very low which, coupled with a general shortage of supply across the country, is expected to keep the housing market at a steady level over the next quarter.

The 16th of May is a very special day on the Evolution Money Calendar – it’s our birthday!

So, this time 6 years ago what was happening…? Well, our colleague James was sitting at his desk (as he is today) but back then he was very excited at the thought of us funding our very first loan, a loan for £750.

It was Monday 16th May 2011 and the business was packaging its very first loan. We had been preparing for this moment for five months and the tension was building… we packaged it, approved it and prepared it for a pre-funding review.

The file was passed to our FD who scrutinised it to within an inch of its life, before he counter-signed it and we were ready to go…

At 16:44 on Monday 16th May 2011 we hit the button and the funds were transferred and that was it, our first loan was funded and Evolution’s journey had begun…!

Fast forward 6 years and what does the business look like today?

Well, we are now a multi award winning, multi-million-pound business…

We’ve outgrown the stationery cupboard we started out in and now employ over 150 people. From that first loan for £750 we have gone on to lend a staggering £134m to over 14,000 customers. That’s certainly something worth celebrating.

One of the highlights of the last six years must be watching how people have grown with the business and seeing new people join. At Evolution Money, we truly do have a brilliant team of people. It’s testament to the business that many of the original team are still here all this time later.

Six years on, as MD, I am still as excited as I was when we funded that first loan. The building blocks have been secured for the future and the business continues to grow from strength to strength.

The future is still for us all to determine and if we work together it will be great. We must remember the founding value of our business, succinctly rolled up in one word – TRUST.

Trust that we are doing the right things every day. Trust from our investors that we are running a compliant and robust business. Trust from our customers that we interact with them in a fair and transparent way, ensuring they are at the heart of everything we do. Trust from our colleagues that we are all working together and that no one individual is more important than the team…. If we achieve this then we will continue to have a great business.

On behalf of myself and the rest of the Directors a huge THANK YOU to both our customers and our team for the journey so far and we look forward to working with you for the next 6 years…

Mat Beaver,

Managing Director

The Financial Conduct Authority (FCA) has proposed new rules which are aimed at tackling the worrying rise in long-term credit card debts, by compelling firms to encourage faster repayments, and in some cases, reducing or waiving interest charges.

What are persistent debts?

According to the FCA, persistent credit card debt affects anyone who has paid more in interest and charges than they have repaid of their borrowing over the course of 18 months. With an estimated 3.3 million people in persistent debt, their new proposals could provide a much needed source of relief.

Andrew Bailey, chief executive of the FCA, highlighted the extreme costs of persistent debt, noting that this was largely deliberate on the part of lenders ‘because these customers remain profitable, firms have few incentives to intervene.’

The new rules

The new guidelines suggest that firms should contact customers who have been in persistent debt for more than a year and a half, prompting them to make faster repayments.

Following a further period of 18 months, firms would be required to propose repayment plans to customers. Those who cannot afford to pay the balance in a reasonable period could then have interest charges reduced or cancelled. The FCA also recommends that firms use the vast amount of customer data available to them to identify those experiencing difficulties and intervene.

The proposals are now in consultation until July 3rd 2017, with the watchdog estimating that it could save customers between £3 billion and £13 billion by 2030.

In the meantime, it’s always worth weighing up every option before you take the plunge with a particular credit card or loan. If you aren’t confident that you’ll be able to pay off the amount you borrow each month, other forms of credit may be more suitable for you.

Given the disparity between surging house prices and annual salary increases, it should come as no surprise that millennials are facing huge difficulties when trying to buy their first home.

First-time buying has never presented such a tough task, which you’d think would deter the millennial generation from seeking home ownership. However, a recent report from HSBC has revealed that an overwhelming number of millennials still dream of owning a home. Almost three-quarters of those surveyed hoping to get a foothold on the property ladder within the next five years.

Alive and kicking

Tracie Pierce, Head of Mortgages at HSBC UK, said: ‘This study challenges the myth that the home ownership dream is dead for millennials in the UK. With three in ten already owning their own home, the dream of home ownership for millennials is definitely alive and kicking.’

While thrifty saving and effective budgeting has helped many to fulfil their dream of owning bricks and mortar, a large proportion of millennial homeowners have inevitably dipped into the bank of Mum and Dad. Thirty-five percent of millennials relied on parental help with their purchase, and over a quarter moved back in with their parents to save for a deposit.

Skipping brunch

The report also revealed that millennials are willing to make considerable sacrifices to own a home. Despite the popular image of millennials as brunch-obsessed spendaholics, almost half of those surveyed (47%) indicated that they would be willing to cut down on their leisure spending.

Thirty-three percent would be prepared to settle for a smaller property, and sixteen percent would even consider delaying having children.

It pays to save

Housing market woes don’t just affect the millennial generation. Four in ten of all non-owners intending to buy revealed that they hadn’t set a budget at all, while forty-eight percent only had a rough budget in place.

Stagnant incomes and a buoyant housing market represent a major obstacle to buying a house, but there are steps which can be taken. Planning early, finding a competitive mortgage and budgeting beyond the purchase price can all help to make your dream of home ownership a reality.

The Darwin group – which offers secured and unsecured loans to customers through Evolution and Progressive Money – is delighted to announce a new funding facility of in excess of £75m which supports the Groups objective of becoming a leading consumer finance brand in the UK.

The award-winning Evolution, ranked as one of the fastest growing finance companies in the UK as recognised in “The Sunday Times Virgin Fast Track 100”, and its sister company Progressive Money, have built up a substantial loan portfolio, having lent more than £120m in just over 5 years.

Joining the original funding partners, NatWest and Shawbrook Bank, are Insight Asset Management and another UK-based private credit manager, all four of whom have significant experience in financing consumer finance lenders and a shared desire to see Evolution and Progressive Money increase market share through both organic growth and the development of new and innovative products.

Steve Brilus, Chief Executive of Darwin said “We are entering an exciting new phase of growth and I am delighted to have such forward-looking and supportive funding partners investing in our business. This funding provides the springboard to enable us to achieve our ambitious plans and to take Evolution and Progressive Money to the next level”.

Evolution and Progressive Money were advised by the Financial Services Corporate Finance team at EY.

Mat Beaver, Managing Director of Darwin said “We are grateful to Nick Parkhouse and the team at EY for facilitating this transaction. They have worked closely with us in understanding our business and our plans, and have supported us throughout the process.”

A recent national report conducted by Halifax has found that people living in nearly one-third of local authority districts in the UK are earning more from simply owning a house than they are from their job.

The report details that surging house prices across the country are rising at a faster rate than many people’s annual salary, particularly when viewed over the course of two years or more. This is the case in 31% of all areas surveyed.

Perhaps unsurprisingly, this trend is most prevalent in London and the surrounding areas. For example, at the upper end of the scale, the average homeowner in Haringey has seen the value of their house shoot up by approximately £91,000 over the course of two years. Roughly, this equals to houses rising by nearly £4,000 per month, which is more than the average homeowner’s monthly income.

First-time buyers

The problem for non-homeowners across the UK

Even though salaries for people in 69% of areas across the UK at least match the rise in house prices, the problems for first-time buyers remain daunting all the same.

Martin Ellis, housing economist at Halifax, said: “Buoyancy in the housing market over the past two to five years has resulted in homes increasing in value by more than total take-home earnings for the average homeowner in many areas, though mostly in southern England’’.

“While it’s no longer unusual for houses to ‘earn’ more than the people living in them, in some places, there are clearly local impacts. Homeowners in these areas can build up large levels of equity quickly but for potential buyers whose wages have failed to keep pace, the cost of buying a home has become more unaffordable during that time.”

It’s hard to believe that we’re almost coming up to a decade since the ‘Great Recession’ that began in December 2007. And although our economy went on to avoid a double dip recession, in the five years that followed, is it fair to say the knock-on effect of the financial crisis is still being felt across the country?

A recent national study led by the Institute for Fiscal Studies suggests that is very much the case, and has even predicted that the average household income in the UK is unlikely to grow for the next two years.

Looking further ahead, the report also suggests that in five years’ time households will only be 4% better off than they are now – which, if true, will mean that UK families face the tightest average income squeeze in 60 years, since World War II.

Getting ahead with your finances

For the average UK household, the risk of financial struggles in the future is not something to put aside until that prospect becomes reality. Chances are, families may find they are up to £5,000 worse off per year than they might expect.

That means forward planning to ensure that any fall in real income doesn’t come as a surprise. Whether means putting a bit of extra cash away now, or preparing to cut down on spending in the next few years – it’s likely to pay dividends in the long run.

With Storm Doris now making her way onto UK shores, the Met Office has issued weather warnings across the country, declaring that the ‘weather bomb’ is likely to cause significant damage to buildings and houses.

In fact, the storm may be far more damaging than first predicted, with experts saying it has since gone through a phase known as ‘explosive cyclogenesis’. There’s no doubt that reported winds of up to 80m/ph will cause havoc among residences in affected areas of the country.

And as your beloved roof panels try to withstand a very tough test, now seems like as good a time as any for those homeowners without home insurance to consider the range of options out there.

Finding a home insurance plan that works for you

For most of us, our home is the single most valuable asset in our possession, which makes a robust home insurance policy essential to protect a property against all manner of eventualities.

Recent national research led by Consumer Intelligence shows that the average cost of home insurance coverage has increased by an average of 1.8% in the past year. This means that a standard policy is likely to cost around £124, and even more for over-50s for whom the increase is as much as 3%.

However, it’s not enough to just go for the cheapest price you manage to find; it always pays to check what is actually covered in each package. From weather damage to theft, there are a wide range of factors to consider – so make sure you double-check the lot before signing on the dotted line!

In what is now an annual tradition, leading comparison website Which? have announced their definitive UK supermarket rankings.

The results follow a nationwide survey in which over 7,000 shoppers from across the country were quizzed on a broad range of customer satisfaction measures, both in store and online.

The best

Renowned upmarket grocer Waitrose topped the overall in-store experience for the third year running, coming in with a customer score of 74% overall. That said, Waitrose were only marginally ahead of both Marks & Spencer and, perhaps surprisingly, Aldi.

But while both Waitrose and Marks & Spencer gained plaudits for their spacious store layouts and helpful staff, Aldi was highly commended for its fantastic value for money and quality own-brand products. Aldi’s prominence also indicates that the average price of goods was a major factor this year.

Meanwhile, Iceland ran away with top spot in the online supermarket rankings with 77% customer satisfaction, another surprise.

The Worst

On the other end of the scale, Tesco, Sainsbury’s and particularly Asda suffered poor in-store scores in comparison. This was largely down to the unavailability of popular items and average food quality compared with other supermarkets.

Asda also ranked joint bottom of the online rankings, along with Sainsbury’s and Waitrose. All things considered, it doesn’t look like it’s been the best year for the bigger supermarket names, with many people seeming to seek an alternative option for their weekly shop.

The results in full

Waitrose – 74% in-store/71% online

Iceland – 69% in-store/ 77% online

Marks & Spencer – 73% in-store only

Aldi – 72% in-store only

Lidl – 72% in-store only

Morrisons – 70% in-store/74% online

Sainsbury’s – 67% in-store/ 71% online

Tesco – 66% in-store/74% online

Asda – 62% in-store/71% online

Ocado – 76% online only

Representative 17.46% APRC (Variable)

For a typical loan of £23,120 over 120 months with a variable interest rate of 17.46% per annum, your monthly repayments would be £442.07. This includes a Product Fee of £2,312.00 (10% of the loan amount) and a Lending Fee* of £763.00, bringing the total repayable amount to £53,047.80. Annual Interest Rates range between 8.6% to 27.87% (variable). Maximum 50.00% APRC. *Lending Fee varies by country: England & Wales £763, Scotland £1,051, Northern Ireland: £1,736.

Think carefully before securing debts against your home. Your home may be repossessed if you do not keep up repayments on your mortgage or any other loan secured against it. If you are thinking of consolidating existing borrowing, you should be aware that you may be extending the terms of the debt and increasing the total amount you repay.